Zero-based budgeting is having its biggest comeback in years. Driven by persistent inflation pressure, rising financial anxiety, and widespread frustration with vague budgeting advice, more Americans are discovering — or rediscovering — a money management system where every dollar gets assigned a specific job before the month begins. This complete guide walks you through exactly how zero-based budgeting works, why it works in 2026's economic climate, and how to set it up step by step — even if you have never budgeted successfully before.

What Is Zero-Based Budgeting?

Zero-based budgeting (ZBB) is a budgeting method where your income minus your expenses equals exactly zero — every dollar is assigned a specific job before the month begins. Unlike traditional budgeting, which tracks spending after it happens, zero-based budgeting plans where each dollar goes in advance.

The core principle is simple: give every dollar a job. When your income arrives, you divide it across your expense categories until there is nothing left to assign. The goal is not to spend all your money — it is to account for every dollar intentionally. If you have $500 left after covering your bills, that $500 goes into savings, debt payoff, or a category you chose deliberately, rather than disappearing into your account with no plan.

This approach differs sharply from the most common budgeting failure: reactive tracking. Most people who try budgeting first write down what they spent after the fact. Zero-based budgeting flips this. You decide first, spend second, and track third. The planning happens before the month begins — not after it ends.

The method originated in corporate finance in the 1970s, where businesses were required to justify every dollar in each new budget period. Personal finance coaches and apps like YNAB adapted the principle for individual households in the early 2000s, and it has remained one of the most recommended systems for people who want genuine control over their money.

Why Zero-Based Budgeting Is Having a 2026 Moment

Inflation has been the defining financial story of the past several years, and 2026 is no exception. Even workers whose wages have kept pace report feeling the squeeze in ways that paycheck-to-paycheck budgeting never adequately addressed. When a $100 grocery trip buys noticeably less than it did two years ago, vague advice like "just spend less" falls flat. People want a system — not a platitude.

Zero-based budgeting answers that need directly. It forces a thorough accounting of every dollar, which means you cannot hide from the categories where your money actually goes. For many people, this honest look reveals spending patterns they did not realize they had — the $14/month subscription they forgot they signed up for, or the category where they consistently overspend by $80.

The personal finance space has also matured. Apps like YNAB, Monarch Money, and Emma have made zero-based budgeting more accessible than ever, with automatic transaction import, category tracking, and mobile-friendly interfaces. The days of managing a complex spreadsheet by hand are optional now. The methodology is the same; the tools are simply better.

On the cultural side, the "loud budgeting" and "financial independence" communities have championed zero-based approaches. There is a growing recognition that financial clarity requires upfront effort — and that budgeting done right is not about deprivation but about intentionality. Zero-based budgeting fits that philosophy better than any other mainstream method.

Zero-Based Budgeting vs Other Methods

Zero-based budgeting is not the only method out there. Understanding how it compares to other popular approaches helps you decide whether it is the right fit — or whether you might combine elements from multiple systems.

Zero-Based Budgeting vs the 50/30/20 Rule

The 50/30/20 rule divides your after-tax income into three broad buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It is a simple framework that requires minimal maintenance once you understand your spending.

The problem with 50/30/20 is that it does not tell you what to do within each bucket. If you spend $600 on needs when your budget allows $700, the rule does not guide you on where to put the extra $100. Zero-based budgeting fills that gap. Every dollar has a home, and there is no ambiguity about where unallocated money should go.

50/30/20 works best for people who have stable income and spending patterns and who mostly want a sanity check rather than granular control. Zero-based budgeting works best for people who want to actively shape their spending and savings behaviour month by month.

Zero-Based Budgeting vs Envelope Budgeting

Envelope budgeting is a cash-based system where you divide physical cash into labelled envelopes for each spending category. When an envelope is empty, you stop spending in that category until the next month.

Envelope budgeting works well for people who respond strongly to physical cash and the tactile reality of watching money leave an envelope. However, it is impractical for a world where most transactions are digital — rent, utilities, streaming services, and most everyday purchases happen online or via card.

Zero-based budgeting achieves the same goal (category-level spending control) without requiring cash. Modern zero-based budgeting apps automatically categorise your transactions and show you how much you have left in each category in real time. You get the discipline of envelopes with the convenience of digital tools.

Zero-Based Budgeting vs Traditional Tracking

Traditional spending tracking — using an app or bank statement to see where your money went after the fact — is the most common approach and the most common failure mode. It tells you what happened; it does not tell you what should happen.

Zero-based budgeting prevents overspending rather than simply documenting it. When you assign every dollar before the month begins, you make conscious choices upfront. Traditional tracking reveals patterns after the fact, which is useful for analysis but does not itself change behaviour.

How to Set Up Your Zero-Based Budget — Step by Step

The setup process takes a few hours the first time you do it, and it becomes faster with practice. Most people can complete their first zero-based budget in 60 to 90 minutes. Here is exactly how to do it.

Step 1: Calculate Your Total Monthly Income

Write down all the money you expect to receive this month after taxes. Include your salary, side gig earnings, freelance income, child support, or any other regular inflow. If your income varies month to month — as it does for freelancers and contractors — use your lowest reliable monthly figure as your baseline. You can adjust upward when you have a good month.

Step 2: List All Fixed Expenses

Fixed expenses are the categories that stay the same every month and that you must pay regardless of other choices. Write them down with their exact amounts:

- Rent or mortgage payment

- Car payment or lease

- Insurance premiums (car, health, renters)

- Phone bill

- Internet service

- Streaming subscriptions (Netflix, Spotify, etc.)

- Gym membership

- Student loan minimum payment

- Child support or alimony

Subtract the total of your fixed expenses from your income. The remaining amount is what you have to allocate to variable and flexible categories.

Step 3: List Variable Spending Categories

Variable expenses are the categories where your spending changes month to month. For each one, write an estimated monthly amount based on your recent spending history — not what you wish you spent, but what you actually spend:

- Groceries — how much did you actually spend last month?

- Gas and transportation — fuel, Uber, public transit

- Utilities — electricity, water, gas (check last month's bill)

- Dining out and takeout

- Entertainment and leisure

- Clothing and personal items

- Household supplies and maintenance

- Medical expenses and prescriptions

Step 4: Assign Every Remaining Dollar to a Savings Goal or Spending Category

This is the core of zero-based budgeting. After covering your fixed and estimated variable expenses, you will likely have some money left over. That remaining amount goes into specific savings or spending categories — not into a generic "miscellaneous" bucket.

Popular categories for this leftover allocation include: emergency fund contributions, retirement account deposits, extra debt payments beyond the minimum, a vacation fund, or a category for irregular expenses like annual subscriptions and car registration.

Step 5: Make Sure Income Minus Expenses Equals Zero

Add up all your category allocations — fixed expenses, variable estimates, and savings goals. The total must equal your total income. If it does not, you have two options: find categories where you can realistically cut spending, or assign the extra money to savings. You do not leave money unallocated. Every dollar gets a job.

Step 6: Automate What You Can

Automation is what makes zero-based budgeting sustainable over the long term. Set up automatic transfers for your savings contributions the day after you receive your paycheck. Automate your bill payments so fixed expenses are covered without you having to think about them. Configure your budgeting app to import transactions automatically so your category balances update in real time.

The less you have to remember to do manually, the more likely you are to stick with the system.

Step 7: Review and Adjust at the End of the Month

At the end of each month, compare what you actually spent in each category against what you allocated. If you overspent in one category, that money has to come from somewhere — typically you reduce the next month's allocation to the category that went over. If you underspent, carry that unused amount forward into the next month's budget.

This monthly review is what continuously calibrates your budget to your real life. After two or three months, your estimated category amounts will become quite accurate.

A Practical Example: $3,500/Month Income

Here is how this works in practice with a realistic income. Suppose you take home $3,500 per month after taxes.

- Rent: $1,200

- Car payment: $350

- Insurance: $150

- Phone and internet: $120

- Subscriptions: $65

- Student loan minimum: $100

- Groceries: $400

- Gas and transport: $150

- Utilities: $100

- Dining out: $150

- Entertainment: $80

- Emergency fund: $200

- Debt extra payment: $200

- Clothing and personal: $75

- Medical: $50

- Household supplies: $75

- Miscellaneous buffer: $35

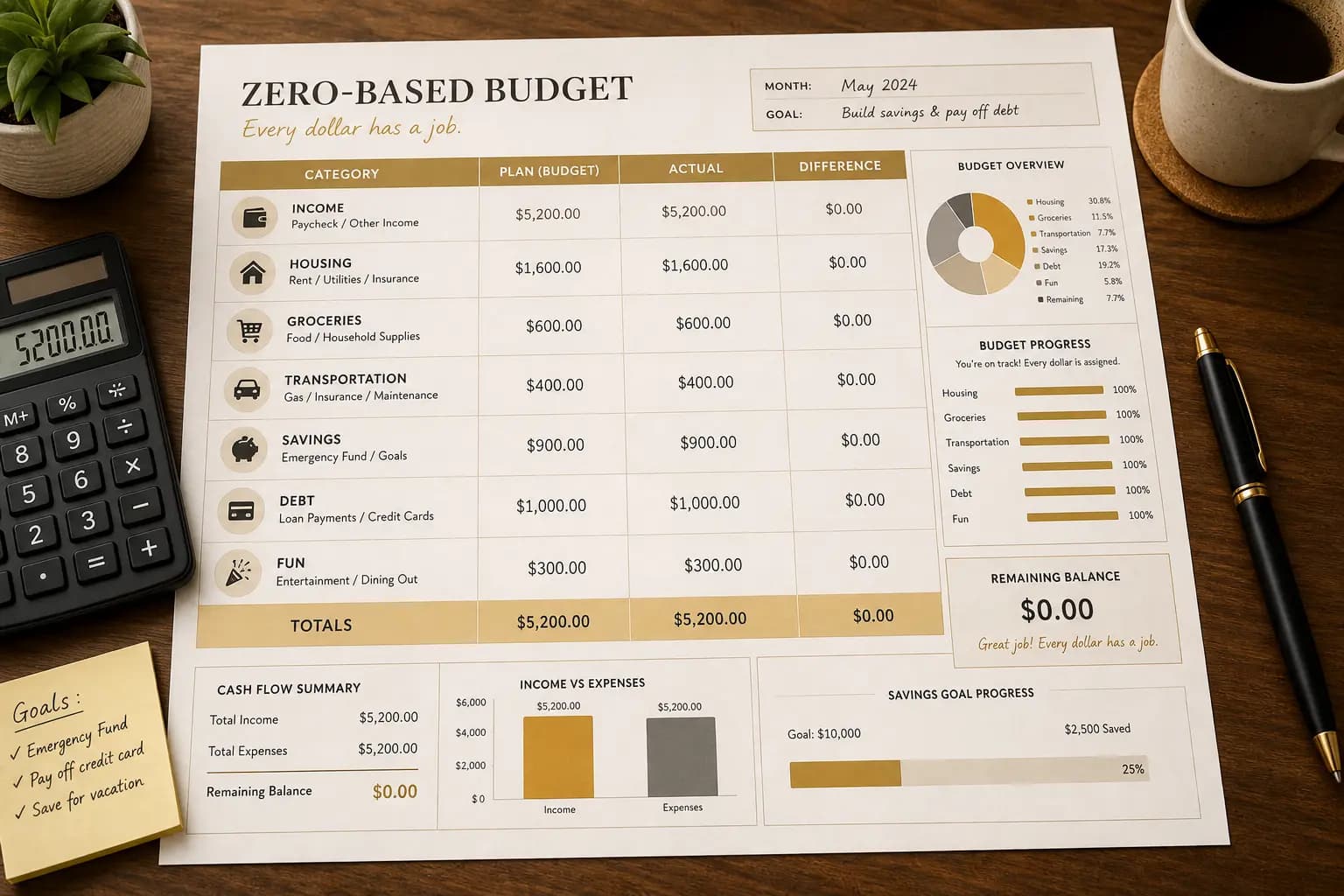

Total allocated: $3,500. Income minus expenses equals zero. Every dollar has a job. This is the zero-based budgeting equation in action.

Zero-Based Budgeting Template and Free Tools

You do not need any special equipment to do zero-based budgeting. Here are the tools that work best in 2026, from simple spreadsheets to full-featured apps.

Recommended Zero-Based Budgeting Apps

- YNAB (You Need a Budget) — The original zero-based budgeting app with robust category management, goal tracking, and educational resources. $14.99/month or $109/year.

- Monarch Money — A modern alternative with夫妻 joint budgeting features, automatic import, and a clean interface. $9.99/month for individuals, $14.99/month for couples.

- Emma — A European-focused app with strong spending categorisation, budget alerts, and a free tier. Useful for those who bank with multiple institutions.

- Copilot — A U.S.-based app with AI-powered categorisation, beautiful dashboards, and joint household support. $12/month or $95/year.

Spreadsheet Template

If you prefer to start with a simple spreadsheet before committing to an app, here is a basic category structure you can recreate in Google Sheets or Microsoft Excel. Create columns for: Category Name, Budgeted Amount, Actual Spent, and Difference. Set up a summary row at the bottom where the sum of Budgeted Amount equals your total monthly income.

The key principle is the same whether you use an app or a spreadsheet: every dollar in your income column gets assigned to a row in the Budgeted Amount column until the sum of that column equals your total income. That equation — income minus budgeted expenses equals zero — is what makes it a zero-based budget.

Setting Up Auto-Transfers

One of the most powerful automation moves you can make is setting up a scheduled transfer from your checking account to a high-yield savings account the day after each paycheck arrives. Even $50 or $100 per paycheck adds up to $1,200 to $2,400 per year with zero ongoing effort. Your savings goal in your zero-based budget becomes automatic.

Common Mistakes to Avoid

Zero-based budgeting has a reputation for being complex, but most of the difficulty comes from avoidable mistakes. Here are the five that trip people up most often — and how to sidestep each one.

Mistake 1: Forgetting Irregular Expenses

Car insurance paid twice a year, annual subscription renewals, holiday gifts, car registration, and dental check-ups — these are the expenses that blow a zero-based budget when they arrive unexpectedly. The fix: create a dedicated "irregular expenses" category and contribute a small amount to it every month. When the bill comes, the money is already there. A good rule of thumb is to set aside 5 to 10 percent of your monthly income for irregular costs.

Mistake 2: Setting Categories Based on Ideals Rather Than Reality

Many first-time zero-based budgeters allocate $200 for groceries when they actually spend $450. When the real number comes in month after month, frustration builds and the budget gets abandoned. The fix: look at your last three months of bank and credit card statements to find your actual spending in each category before you set your budget amounts. Base your budget on reality, not aspiration.

Mistake 3: Not Building in a Guilt-Free Zone

Zero-based budgeting can feel restrictive if every dollar is spoken for in a way that leaves no room for spontaneous enjoyment. The result is often a reaction — a big unplanned purchase that derails the whole month. The fix: create an explicit "guilt-free spending" category, however small. $50 for coffee, takeout, and entertainment is not going to break your budget, and having it there means you do not feel deprived.

Mistake 4: Over-Complicating the Categories

It is tempting to create a category for every possible expense — "Asian restaurants," "Italian restaurants," "fast food," "coffee shops," "groceries — produce," "groceries — protein." But more categories mean more tracking work and more categories that go over budget in confusing ways. Start with ten to fifteen broad categories. You can always split a category later if you find you need more detail.

Mistake 5: Giving Up After One Bad Month

Every budget — even a well-planned zero-based budget — has months where a category goes over. This is not a failure of the system. It is simply data. If you overspent on dining out by $90 in January, you reduce the February allocation or you accept that February's dining budget is lower to compensate. One off-month does not mean the system does not work. It means the system is telling you something about your real spending habits.

Signs Your Zero-Based Budget Is Working

Zero-based budgeting produces measurable signs of success. If you are doing it right, you will notice these changes within the first two or three months.

- You know where every dollar is going before the month starts — not after it is gone

- You are hitting savings goals consistently because savings is a line item, not an afterthought

- Month-end surprises are fewer. You are not shocked by bills you forgot were due

- You feel in control of your money rather than anxious about it

- You can answer the question "how much can I spend on this?" with a specific number from your budget

- You are paying down debt faster because extra payments are built into your categories

The ultimate sign of success is a month where your actual spending matches your budget closely — not because you were perfect, but because the categories reflected your real life accurately. That alignment between plan and reality is what zero-based budgeting is designed to produce.

Zero-Based Budgeting FAQ

Zero-based budgeting is a budgeting method where your total monthly income minus your total allocated expenses equals exactly zero. Every dollar is assigned to a specific category before the month begins, ensuring no money is left unplanned. This differs from traditional budgeting, which typically tracks spending after it has already occurred.

Start by calculating your total monthly after-tax income. Then list all your fixed expenses and estimate your variable spending for each category. Assign every remaining dollar to a savings goal or spending category until your allocated total equals your income. Use an app or spreadsheet to track your categories, and review your actual spending against your plan at the end of each month.

Yes. Research from the Consumer Financial Protection Bureau (CFPB) consistently shows that people who plan their spending in advance — the core principle of zero-based budgeting — have significantly higher rates of financial well-being and lower rates of financial stress compared to those who track spending after the fact. The method works because it forces intentional decision-making before spending happens rather than reactive analysis afterward.

The main advantages are complete financial clarity, intentional allocation of every dollar, and the ability to direct money toward savings and debt payoff goals before spending it. The main disadvantage is that it requires more upfront planning time than simpler methods, and it can feel restrictive if you do not build in a guilt-free spending category. It also requires regular monthly reviews to keep category estimates accurate.

The 50/30/20 rule divides your income into three broad percentages: 50% needs, 30% wants, and 20% savings. It does not specify how to allocate within each bucket. Zero-based budgeting requires you to allocate every single dollar to a specific category, producing a more detailed and granular financial plan. Zero-based budgeting offers more control but requires more effort to set up and maintain.

The initial setup typically takes 60 to 90 minutes for your first month, including reviewing bank statements, categorising past spending, and allocating every dollar. After your first month, most people can update their budget in 20 to 30 minutes. With an app that automatically imports transactions, the ongoing maintenance is significantly faster.

Yes, and it is actually one of the best methods for variable income. Base your budget on your lowest reliable monthly income figure. When you earn more in a given month, assign the surplus to savings goals, extra debt payments, or your irregular expenses category. When you earn less, you reduce allocations from non-essential categories. This prevents the feast-or-famine cycle that variable-income earners often experience with fixed budgeting methods.

Conclusion

Zero-based budgeting is simple in principle and powerful in practice. The entire method rests on one equation: income minus expenses equals zero. Every dollar has a job, and every job is intentional. In 2026's economic environment, that level of clarity is not just nice to have — it is essential.

The setup takes a couple of hours. The reward is months and years of knowing exactly where your money goes, hitting savings goals consistently, and feeling genuinely in control of your financial life. If you have tried budgeting before and lost momentum, zero-based budgeting is worth a second look. The method is the same; the tools in 2026 are better than they have ever been.