If you've ever set up a budget, felt determined for three days, then watched it fall apart by the second week — this article is for you. New research from Fidelity Investments confirms what many budgeters quietly suspect: the reason budgets fail has nothing to do with being bad with money. It has everything to do with hidden psychological and structural triggers that are built into the way most people set up their budgets in the first place. Understanding these triggers is the first step toward building a budget that actually lasts.

Most people assume that when a budget fails, it fails because of a willpower problem — they weren't disciplined enough, they lacked control, they made too many impulse purchases. But Fidelity's 2026 research on budget failure patterns tells a very different story. The data shows that the majority of budget failures are triggered by specific, predictable structural flaws in how the budget was set up — not by the person's character or financial knowledge. The good news: once you know the triggers, you can fix them.

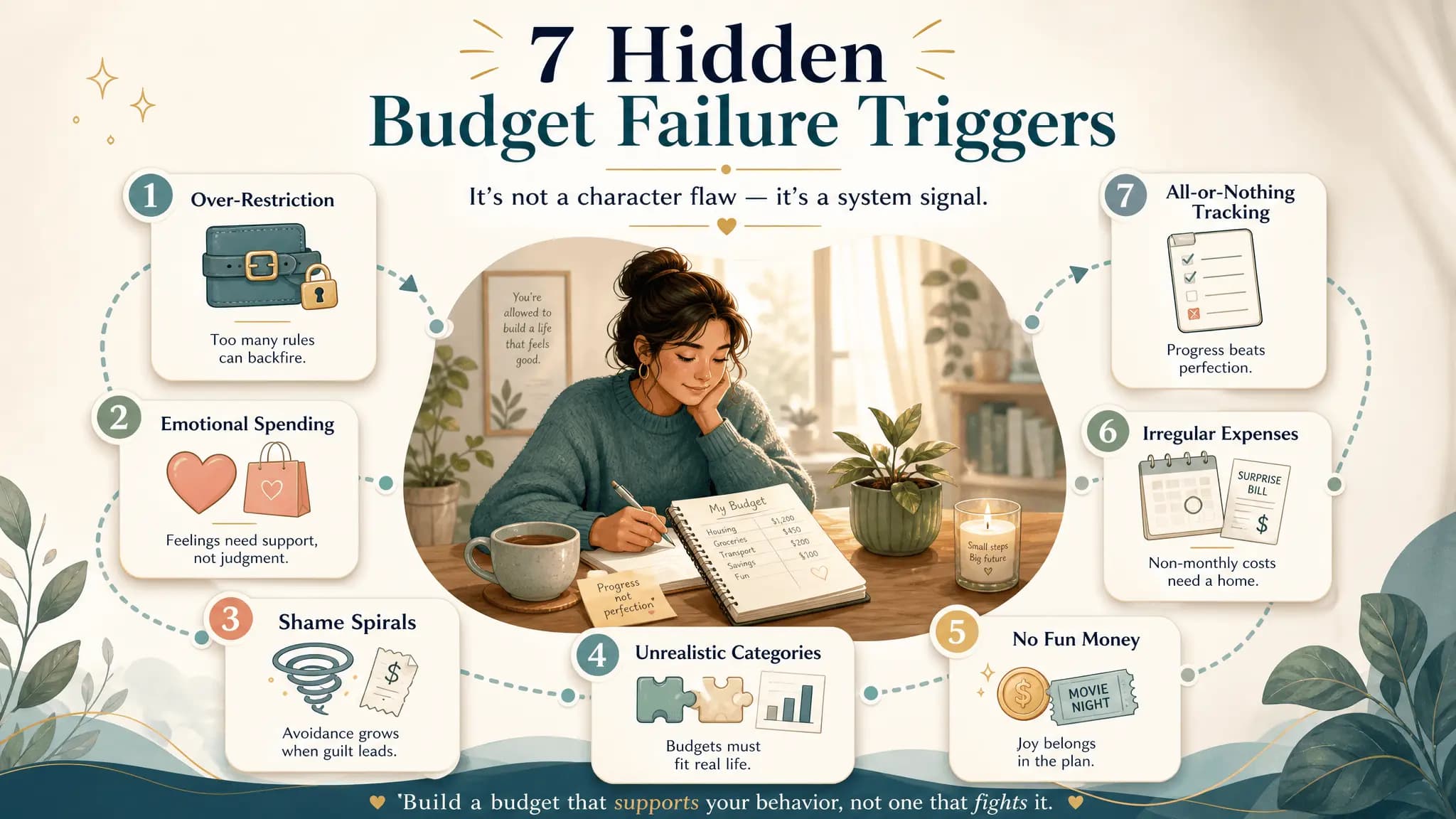

Fidelity's research identified seven distinct patterns that consistently predict when and why a budget will break. These aren't random mishaps — they're systematic failure points that appear again and again in the data. Recognizing them in your own budget is the first real step toward building something that works.

The single most common budget failure trigger is setting spending limits that don't reflect how you actually live. If your budget assigns $150 a month for groceries but your actual household spending runs closer to $280, the budget isn't a guide — it's a daily reminder of failure. This creates a psychological pattern called budget fatigue, where each trip to the store becomes a微量 shame spiral. By the third week, many people simply give up entirely, not because they lack discipline, but because the numbers were never realistic to begin with.

The fix: track your actual spending for 30 days before setting any budget limits. Use that real data to set categories that reflect your life — not an idealized version of it. Give yourself permission to adjust as you learn.

Many budget templates ask you to estimate 'average' monthly spending. The problem is that your actual spending isn't average — it's seasonal, unpredictable, and full of one-off purchases that don't repeat monthly. A budget built on averages will fail the moment an irregular expense appears: a car repair, a medical bill, a birthday gift that doesn't come every month. These irregular costs don't fit neatly into any category, so they break the whole system.

The fix: create dedicated sinking fund categories for irregular but predictable expenses — annual subscriptions, holiday gifts, car maintenance, vet visits. Budget a small amount into each category every month so the money is already there when the expense hits.

Building on the previous trigger — one-time expenses are one of the fastest budget killers. Things like annual insurance premiums, back-to-school costs, or unexpected home repairs aren't monthly events, so they don't show up in most people's budget categories. When they hit, they wipe out an entire month's progress in one transaction. The emotional response to this is often shame ('I ruined my budget again') even though the expense was completely predictable and normal.

The fix: list every one-time expense you can think of over the next 12 months and assign each a monthly savings target. Even $20 a month per category builds into meaningful coverage by the time the expense arrives.

Fidelity's research confirms what behavioral economists have long understood: emotional states are among the strongest predictors of budget failure. Stress, boredom, loneliness, celebration, and even revenge can all trigger spending that has nothing to do with actual need. A tough day at work leads to an online shopping cart checkout. A fight with a partner leads to a 'I deserve this' treat. These spending episodes aren't rational — and no budget spreadsheet can prevent them because they bypass the logical part of your brain entirely.

The fix: build a 'pause and plan' habit before any non-essential purchase over a small threshold. Identify your specific emotional spending triggers and create friction between the trigger and the purchase. This isn't about restriction — it's about creating a gap between impulse and action.

Setting up a budget is an event. Sticking to it is a practice. Most budgeters treat their budget like a set-it-and-forget-it system — they enter numbers once and don't look again until something goes wrong. Without a regular check-in habit, small overspending in week one turns into week two overspending, which turns into month-end panic. The budget stops being a tool and starts being a source of anxiety that people avoid looking at.

The fix: schedule a weekly budget check-in — even just 10 minutes on Sunday evening. Review what you spent, what's left in each category, and what adjustments you need to make for the coming week. This keeps the budget alive as a living tool rather than a quarterly guilt trip.

This is the trigger that Fidelity's research flags as one of the most psychologically damaging: shame spiral syndrome. It starts when one budget overspend triggers a wave of negative self-talk. The shame itself becomes so uncomfortable that people stop tracking entirely — which paradoxically leads to more overspending, because there's no longer any awareness of where money is going. The budget didn't fail because of the original overspend. It failed because shame caused the person to disengage from the system entirely.

The fix: build a 'budget reset' into your system from day one. Give yourself a written rule that says 'if I go over in any category, I note it, adjust, and move on — no shame.' Normalize budget failure as a data point, not a character judgment.

Not all budget methods are created equal — and not every method works for every personality type. If you're someone who needs flexibility and hates feeling constrained, a zero-based budget where every dollar is assigned a job will feel suffocating. If you need strict guardrails, a simple 50/30/20 framework may be too loose. Fidelity's data shows a strong correlation between budget failure and personality-type mismatch.

The fix: understand the main budget types and match them to your personality. The 50/30/20 rule is great for flexibility-first personalities. Zero-based budgeting works well for detail-oriented planners. Envelope budgeting suits people who benefit from physical, visual spending controls.

If your current budget has already failed, don't wait for 'Monday' or 'next month' to start over. Here's a practical three-step process for getting back on track right now.