Executive summary: Annual bills feel expensive mostly because they arrive all at once, not because they are unexpected. A simple monthly system helps households spread those costs across the year, so insurance, registrations, holidays, and home repairs stop blowing up the budget.

Why annual bills throw off a personal budget

Most monthly budgets handle rent, groceries, and utilities well enough. The trouble starts when a bill shows up once or twice a year, because that cost is easy to forget during normal monthly planning. Car insurance, school fees, annual subscriptions, holiday spending, or routine home maintenance can wipe out progress fast when they are treated like surprises.

That is why learning how to budget for annual bills matters. The goal is not to predict every penny perfectly. It is to turn irregular expenses into smaller monthly amounts you can prepare for without scrambling.

Start by listing every irregular bill you expect this year

Look back through the last 12 months of bank statements, budgeting apps, email receipts, and calendar reminders. Pull out anything that repeats quarterly, twice a year, seasonally, or once a year. People usually remember the big bills and miss the smaller ones that quietly stack up.

- Car insurance premiums, registration fees, and annual road-tax payments

- Homeowners or renters insurance, property taxes, and HOA dues if they are not paid monthly

- Holiday spending, birthdays, school fees, and back-to-school shopping

- Medical deductibles, vet care, or routine checkups you know are likely to happen

- Annual subscriptions, domain renewals, warehouse memberships, and home maintenance like AC servicing

Use realistic numbers, not best-case guesses. If a bill has been creeping up, round up a little so the budget can absorb the increase.

Convert each annual bill into a monthly savings target

Once you have the list, write the expected yearly amount for each expense and divide it by 12. That gives you the monthly amount to set aside. The bill may come once a year, but the funding happens every month.

- Write the bill name and the expected total amount.

- Add the due month or rough timing.

- Divide the total by 12 to get the monthly savings target.

- Add that amount to your budget as a fixed monthly line item.

Example: If car insurance costs $1,200 a year, save $100 a month. If holiday spending is usually $600, save $50 a month. If annual home maintenance averages $480, save $40 a month.

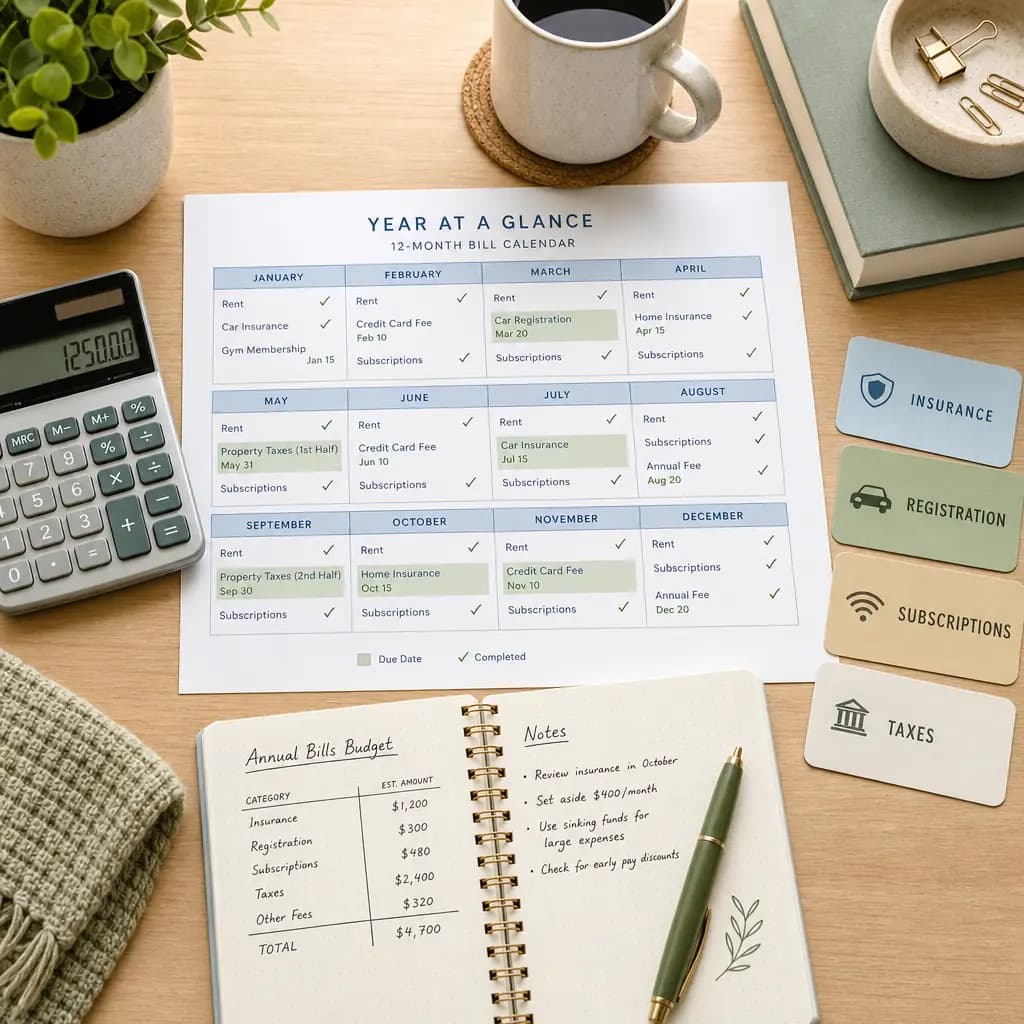

Use a calendar so due dates do not sneak up on you

A simple annual bill calendar helps you see when several expenses land close together. A spreadsheet works. A budgeting app works. A paper planner on the fridge works too. The format matters less than being able to spot heavy months early.

- Add each annual or seasonal bill to the month it is due

- Set reminders 30 days ahead for larger payments

- Note both the expected total and the monthly amount you are saving

- Review the calendar during your regular monthly budget check-in

This is where the system gets practical. If you can see that travel, insurance, and holiday costs all pile up in the same quarter, you have time to cut back somewhere else before the pressure hits.

Keep annual-bill savings separate from spending money

The system only works if the money does not get absorbed into everyday spending. Some people use a separate savings account. Others keep sinking-fund categories inside a budgeting app. Either way, the point is the same: money for annual bills should stay visible and hard to accidentally spend.

If your income changes from month to month, fund the most urgent categories first. Then use stronger months to top up the rest.

Prioritize the bills that would hurt most if they landed tomorrow

If there is not much room in the budget yet, start with the bills that create the biggest stress or the biggest consequences. Insurance lapses, tax payments, and school-related costs usually matter more than a streaming subscription renewal.

- Cover essential bills first, such as insurance, taxes, and required registrations.

- Next, fund predictable household costs like school fees, repairs, and medical expenses.

- Then add lower-priority categories such as gifts, travel, or optional subscriptions.

- Cut anything you keep renewing without getting much value from it.

What to do if you are starting late

A lot of people only build this system after an annual bill already caused a problem. That is fine. Start with the next big expense on your calendar and build a partial reserve now instead of waiting for a clean restart next year.

- Focus on the next bill due, not every category at once

- Save a smaller monthly amount if the full target is unrealistic right now

- Trim low-value spending for a few months to create space

- Use bonuses, refunds, or extra income to catch up faster when possible

Even an imperfect reserve is better than treating a predictable expense like an emergency.

Common mistakes when budgeting for annual bills

- Forgetting smaller renewals and one-off fees that recur every year

- Using outdated amounts and saving too little

- Keeping reserve money mixed in with daily spending cash

- Ignoring due dates until the bill is already close

- Trying to fund every category perfectly from the start

A quick monthly review is usually enough to keep the plan accurate. Update totals, remove expenses you no longer have, and adjust categories that cost more than they used to.

FAQ

What counts as an annual bill?

Any predictable expense that does not happen every month can count, including insurance, registrations, taxes, subscriptions, school costs, holidays, and planned maintenance.

Is this the same as a sinking fund?

Yes. Budgeting for annual bills usually means creating sinking funds so you save a little each month for irregular expenses.

Should I use a separate account for annual bills?

It often helps. A separate savings account or clearly labeled budget categories make it easier to protect that money from everyday spending.

What if I cannot fully fund every annual bill yet?

Start with the most urgent or essential expense first, build partial reserves, and add more categories as your budget gets more stable.

How often should I review these categories?

A short monthly review is enough for most households. Check upcoming due dates, confirm the amounts still look right, and adjust as needed.

Pick one annual bill today, divide it by 12, and add that amount to next month's budget. Once you set up one category, the rest of the system gets much easier to maintain.