Budgeting for childcare gets easier when families separate one-time setup costs from the monthly bill, then add realistic buffers for backup care and rate increases. This guide gives parents a practical framework to total daycare, nanny, preschool, and emergency-care costs without guessing. It also shows where tax breaks and family budget adjustments can reduce the pressure.

What a childcare budget should include

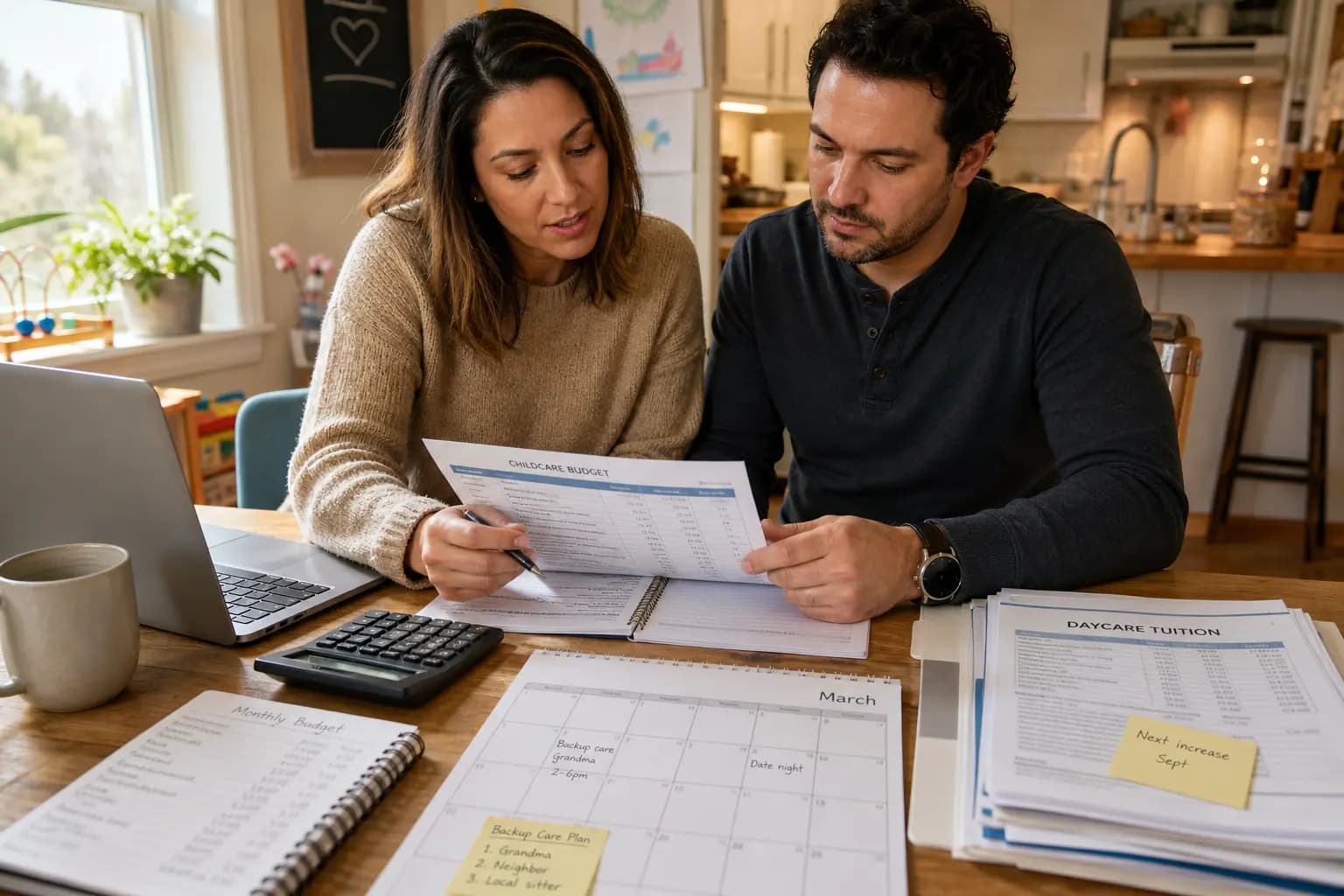

A childcare budget is more than the weekly daycare number. It should cover the full cost of care so you can plan for routine bills, one-time setup fees, and the surprises that show up once care starts.

- Monthly tuition or caregiver pay for daycare, nanny care, nanny share, preschool, or after-school care

- One-time startup costs like registration fees, deposits, waitlist fees, and supplies

- Extra costs such as late pickup charges, field trip fees, meals, or diapers if they are not included

- Backup care for sick days, school closures, holidays, or schedule changes

- A buffer for annual rate increases and changes in care needs as your child gets older

Thinking in total cost instead of tuition alone helps families avoid getting blindsided by the first few months of care.

Separate startup costs from monthly care costs

The easiest way to budget for childcare is to split the numbers into two buckets: one-time setup costs and ongoing monthly costs. That keeps a large deposit or registration fee from distorting your normal monthly budget.

Startup costs to total first

- Registration or enrollment fees

- Security deposits or tuition deposits

- Application fees or waitlist fees

- Supplies, uniforms, bedding, bottles, or lunch gear

- Transportation setup if you need a different commute or pickup plan

Monthly costs to estimate next

- Base tuition or caregiver wages

- Meals, diapers, or activity fees not included in tuition

- Transportation or fuel related to drop-off and pickup

- After-school coverage or extended-hour fees

- A small monthly amount for future rate increases

If you are expecting a baby, build both buckets before the first invoice arrives. That gives you time to save instead of trying to absorb every new expense at once.

Estimate your base monthly childcare bill

Start with the care option you are most likely to use. Get actual quotes when possible, then build your monthly estimate around the schedule your family will really follow.

- Daycare: Use tuition for your child’s age group and ask whether meals, diapers, and early drop-off are extra

- Nanny or nanny share: Include hourly pay, payroll taxes if applicable, and any guaranteed hours

- Preschool or part-time care: Count tuition plus wraparound care if school hours do not match work hours

- After-school or summer care: Budget separately if your child’s needs change through the year

For a cleaner plan, use the highest normal month rather than the cheapest possible month. A realistic number protects the rest of your household budget.

Add backup care, sick days, and late fees

This is where many families underestimate childcare costs. Even reliable care plans break down sometimes, and those backup arrangements can cost real money.

- Keep a backup-care fund for babysitters, drop-in care, or family help you may need to reimburse

- Budget for sick-day coverage if daycare rules require your child to stay home

- Add possible late pickup fees if your work schedule is tight or commute times change

- Include missed-work costs if unpaid time off is the only fallback option

A small reserve is usually easier to manage than scrambling every time your normal routine breaks.

Plan for rate increases and schedule changes

Childcare costs rarely stay flat forever. Rates often rise yearly, and your family’s schedule may change when work hours shift, a second child arrives, or school calendars change.

- Add a monthly buffer for future tuition increases

- Review whether infant, toddler, and preschool rates differ before you assume costs will fall quickly

- Rework your plan if one parent changes jobs, returns from leave, or moves to a different schedule

- Budget ahead for summer care, school breaks, or longer care hours when needed

This keeps your childcare budget flexible enough to survive real life, not just the ideal version of it.

Use tax breaks and employer benefits if available

Tax support will not erase childcare costs, but it can lower the pressure on your monthly budget. Check what applies before you finalize your numbers.

- Dependent Care FSA if your employer offers it

- Child and Dependent Care Credit if you qualify

- State childcare subsidy or assistance programs if your household is eligible

- Employer childcare stipends, backup-care benefits, or flexible work arrangements

Treat these benefits as helpful offsets, not permission to ignore the real cost of care. Build the budget first, then subtract reliable support.

How to budget for one child vs multiple children

Families with more than one child usually need a layered plan. One child might be in infant care while another only needs after-school coverage, so the monthly total can swing more than expected.

- Price each child separately by age group and care schedule

- Ask about sibling discounts, but do not assume they will be large

- Keep one shared backup-care fund for the household

- Recalculate transportation, food, and supply costs as each child’s routine changes

A per-child breakdown makes it easier to see what may change next year and where you need extra savings now.

What to do if childcare is too expensive right now

If childcare takes a painful share of your income, the answer is not shame. It is a clearer decision process.

- Compare daycare, nanny share, family care centers, and part-time combinations in total monthly terms

- See whether flexible work hours can reduce paid care hours without increasing stress elsewhere

- Trim lower-priority budget categories temporarily while care costs are highest

- Use sinking funds for annual childcare costs so they do not hit one month all at once

- Review tax credits, FSAs, and local support programs before assuming the full cost is fixed

The goal is to build a workable plan for this season, even if it is not your forever setup.

A simple monthly childcare budgeting formula

Use this formula as a quick check: base monthly care + monthly extras + backup-care reserve + future-rate buffer = your real childcare budget. Then compare that number to the rest of your household plan so you can adjust groceries, savings, debt payoff, or discretionary spending intentionally.

FAQ

How much should I budget for childcare each month?

Budget for the full monthly cost of your likely care setup, then add extras like supplies, backup care, and a small rate-increase buffer. The right number is your real total cost, not just advertised tuition.

What is the difference between daycare cost and total childcare cost?

Daycare cost usually means the base tuition. Total childcare cost includes tuition plus deposits, registration fees, supplies, late fees, backup care, and schedule-related extras.

Should I include backup care in my childcare budget?

Yes. Backup care is one of the most common budget gaps for families. Even a small monthly reserve can prevent surprise costs from derailing the rest of your budget.

How do I budget if childcare takes most of one paycheck?

Start with the real total cost, then compare care options, adjust other budget categories, and check tax credits or employer benefits. A high-cost season may require a temporary household reset, not a perfect long-term answer.

What tax breaks can help with childcare expenses?

Many families should review the Dependent Care FSA, the Child and Dependent Care Credit, and any state subsidy programs they may qualify for. Use the benefits you can count on, but build your budget around the actual costs first.

Before the first childcare invoice arrives, total your startup fees, estimate your real monthly care cost, and build a backup-care reserve. A clear childcare budget now can protect the rest of your family finances later.